Whenever people say about governance, it reveals many things including internal control. Inter related and sequential procedures or processes which are governed by the rules, regulation and the other relevant prevailing laws, give the true sense for the concept of governance. Apart from these elements, Accountability towards performance, control mechanism and also the attitude of the people associated within, are also considered as the vital components of governance.

The importance of the governance cannot be ignored. Neither the relevance of governance can be overlooked in various sectors like corporate sector, social sectors, politics and even in government itself, nor can be considered as the easy task to assure regarding compliance because of its practical difficulties, rather it can only be optimized by the use of resources to comply control and compliance. Therefore in developing countries like Nepal, everywhere there is question of accountability and control. It has to be noted that single person and single process can not establish the governance. If the processes or the procedures flow within the framework regulated by the governing standards then only governance can be assured. Therefore, People, processes or procedures and standards are the vital elements and the positive inter relation of these elements give the governance.

The term “Governance” in corporate sector, specifies the ability of an organization to be able to control and regulate its own operation so as to avoid conflicts of interest related to the beneficiaries (shareholders) and people involved in the company. Controlling and regulating the operations, minimizing the conflicts produced by the interest of the shareholders and the people involved in the operation within the organization is not an easy task. As a risk, organization should first identify the areas where are the highest possibilities of being conflict of interest. It can only be possible with the help of information in the organization. That is why, it is said that the information system within the organization is the key to implement the governance.

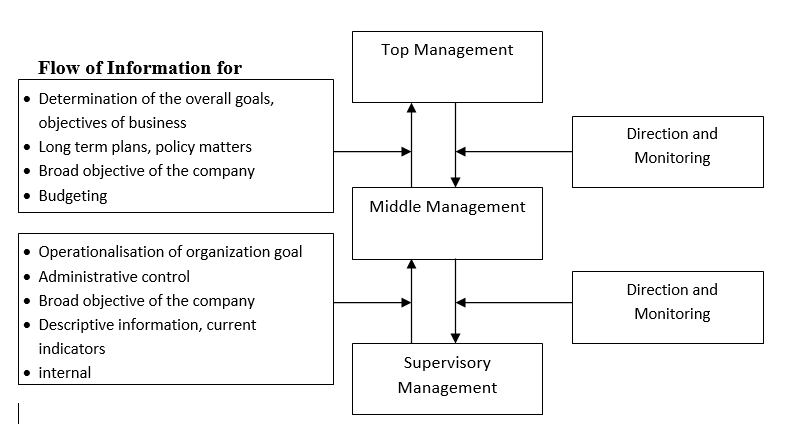

In the organization there are varieties of information which may or may not be useful to attain the objective of the organization. The information which really adds value in decision making irrespective of the layer of management is important within the organization. According to the Koontz, O’Donnell and Brech, management is divided into three levels as top level, middle level and supervisory level. The division is basically on the basis of tasks performed, authority and degree of accountability. Managements take decision regarding their job or the organizations’ benefits in various moments which are initiated and later supported by information available. The information required for this varies depending upon the management level within the organization.

Therefore, the information required for the management is management information and if there is a system or a defined standard to flow the information required to management, between different layers of management, it is called as management information system. In modern world, we cannot imagine information without technology. The introduction of the computer and advent of the Internet has changed the way we live these days. It is not only for an individual but also for corporate.

Information technology and management therefore plays a vital role to the extent that timely access to Information could save a life while improper management of Information could lead to huge problems and losses of opportunities. In terms of corporate governance and financial reporting, the financial implications of these losses could be great on corporate entities when quantified in monetary terms and this has led several companies to invest in finding better ways of improving on information systems.

Internal information is more important than external information in terms of governance because governance simply requires internal control in the process and procedures that happened within the organization while functioning. Such information as needed to know the control system the information required to middle management can only be obtained from internal sources. Internal control system within an organization is the backbone of the governance since the control mechanism assures the compliance. Internal control identifies and assesses operating controls, financial reporting, and legal/regulatory compliance which are the components of governance. Internal control consists of five interrelated components as follows:

- Control (or Operating) environment

- Risk assessment

- Control activities

- Information and communication

As a component of internal control, information and communication not only help to ensure the governance but also minimize risk. Better information leads to increasing of the company’s reputation on the market, because it is more visible the manifestation of quality in its administration and management. Therefore, it is clear the fact that in the own interests, the companies must, first of all, to substantially standardize its information management system that attempt to regulate the organization’s activity and to communicate clearly, transparent and direct all the information necessary to governance. For example reconciliation is a comparison of different sets of data to one another, identifying and investigating differences, and taking corrective action, when necessary, to resolve differences. Reconciling monthly financial reports from the Accounting Department (e.g., Statement of Accounts, Ledger Sheets, etc.) to file copies of supporting documentation or departmental accounting records is an example of reconciling one set of data to another. This control activity helps to ensure the accuracy and completeness of transactions that have been charged to a department’s accounts.

Either the practices of reconciliation activity without circulating reports to relevant department or the reconciliation itself without obtaining proper reports/documents from relevant department never give the accurate and complete scenario so that the management cannot relay and cannot ensure governance/control. Therefore, in the organization, without standardized information system, governance cannot be established. If there is a system in which various departments, branches or even various reporting centers give regular information, management can easily take decision on that basis. Besides this, it will also help to take necessary measures to maintain the control mechanism wherever management feels necessary in terms of compliance.

The governance with full information system is not only required internally but also required to the governing institutions. On the basis of the information/reporting by the organization to those institutions, governing institution will make policy to monitor those organizations. The frequency of information/reporting within the organization is equally importance to assure governance. Therefore, organization can not comply the governance without maintaining the proper information system within it. The cost that may be incurred due to non compliance of governance or the risk arising from not having the proper governance within the organization is far more than the cost incurred to establish the information system within organization.